Buffalo Groupe Makes Big Moves in Research with Placer.ai

Buffalo Groupe—along with Longitudes Group and Sports Marketing Surveys USA which comprise its Research division—has long been an industry leader in golf and other sport research. Historically, we have used traditional forms of research to gather data and learn more about sports participation than any other group in the industry. Last year, Buffalo Groupe leveraged Placer.ai and its movement data to learn more about sports participation, spending, and marketing.

What Is Placer.ai?

Placer.ai collects movement data through the GPS tracking we use on our phones all the time. The data is obtained from hundreds of partner mobile applications that collect data from mobile devices across various categories (i.e., coupons, travel, games, etc.), which generate a diverse panel of more than 25 million monthly average users being tracked. All partners ensure compliance with privacy laws and regulations in their data collection practices. Placer.ai uses machine learning and advanced algorithms to accurately estimate visits to locations across the United States.

How Does Buffalo Groupe Put It to Use?

One example of how Buffalo Groupe has leveraged this data collection for our golf clients is by geofencing over 4,000 golf courses, 260+ off-course golf retail locations, 162 golf entertainment venues (such as X-Golf or TopGolf), and 1,344 sporting goods stores. We have also begun to geofence tennis courts, pickleball courts, skateparks, bike paths, tennis/pickleball retail, and running retail locations to get a pulse on movement in even more outdoor sports.

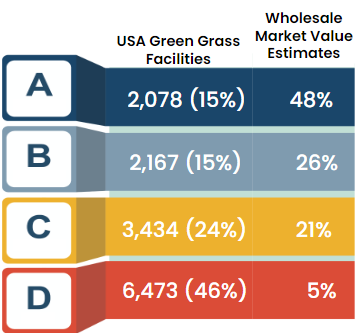

Across the golf courses we track, we classify every facility as A, B, C, or D. These are determined by analyzing 20 years of rounds and revenue volumes, primarily retail sales history, green fees, Golf Advisor ratings, and self-reporting by the pro shop. A-rated facilities are some of the highest-rated golf courses in the nation holding robust and vibrant retail space. 70% of A-rated facilities are private compared to the national average of only 30% of golf facilities being private. Each step down from A-rated takes a step down in retail sales, course rating, and rounds and revenue down to D-rated facilities which consist of primarily public and 9-hole golf courses. 51% of D-rated facilities are 9-holes compared to the national average of 26%.

A Snapshot of Golf Trends Uncovered by Placer.ai Data

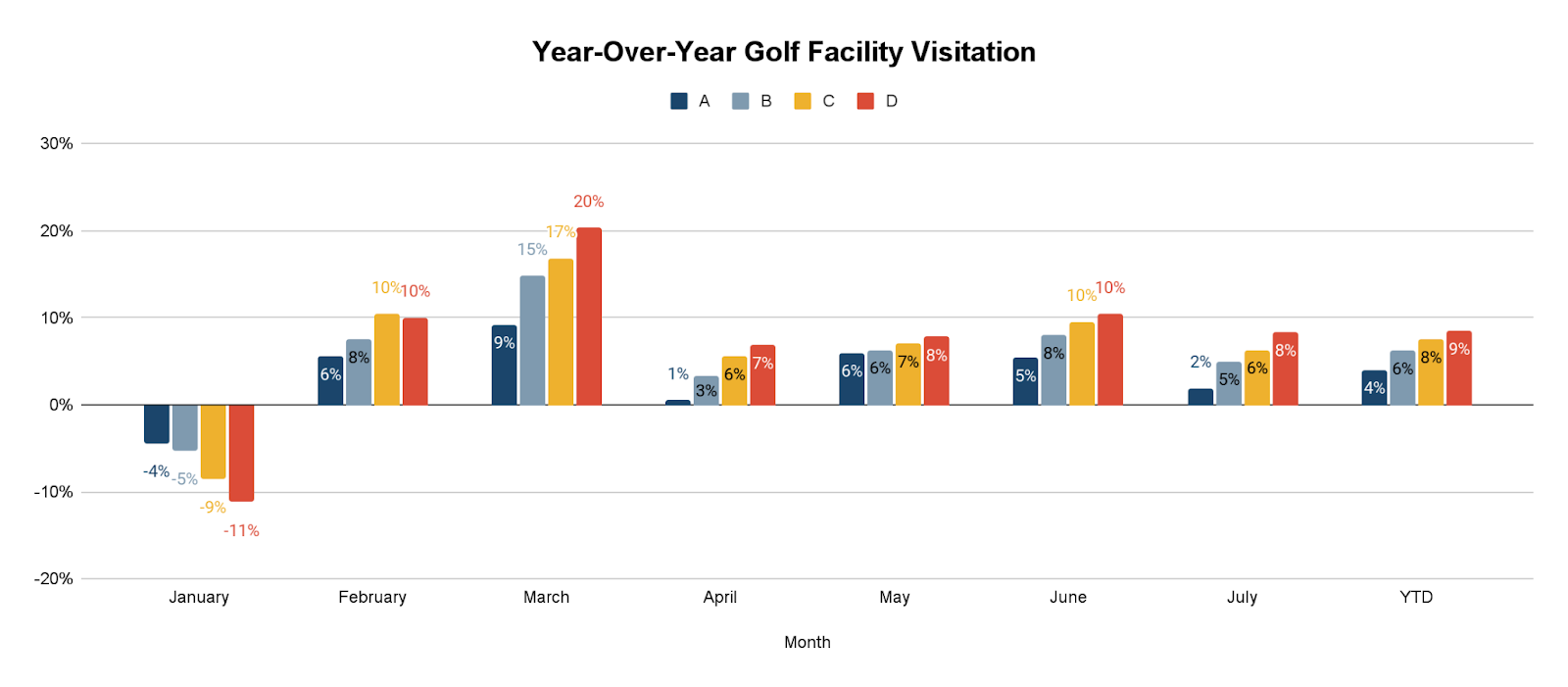

In 2023 we saw the most rounds played in golf history with over 500 million rounds and at golf facilities where we are tracking movement, we have continued to see extremely positive results with a total increase in visitation 2024 YTD by 5.9% year over year. This has been highlighted by increases in visitation by at least 4.0% across each A-D rating with the highest increase in visitation coming from D-rated facilities with an 8.5% increase.

Although you may initially think that an increase in D facility visitation might not be as good for the game as A facility visitation, there are actually a few reasons why this is a very positive sign for the future of golf. D facilities typically house families, beginners, and kids picking up the game. These golfers increasing their visitation should lead to a positive reaction up the food chain all the way to the A facilities as these younger and beginner golfers continue to play the game. There is also a higher volume of D-rated facilities, so a higher YTD visitation percentage in such a large number of facilities means more golf across the country in general.

Many beginner golfers are getting interested in golf by starting at an entertainment venue before moving to the golf course at a 9-hole course. At entertainment venues such as X-Golf or TopGolf overall location visitation has increased 8% year over year through mid July according to data from Placer.ai.

At golf retail locations like Golf Galaxy, PGA TOUR Superstore, and more, we have seen the same trend. Although it may or may not lead to an increase in spending, we can say for sure that the increase in visitation to golf courses and entertainment venues has correlated with an increase in visitation to retail. Across 363 off-course retail locations where we are tracking movement, visitation increased by 5.7% vs 2023. These were highlighted by 11.0% and 11.7% increases at Club Champion and Golftec, respectively, showing golfers are still looking to improve their game.

Beyond Golf

However, movement data does not stop at the golf course. It follows the visitor home, allowing us to learn about the visitors themselves and their households. By using an anonymized home address down to the block, we are able to accurately estimate and aggregate the demographics, spending habits, brand and channel preferences, and even the favorite influencers of visitors to any location. For example, we have learned that in 2024 through mid-July the median household income of visitors to A-rated facilities is more than $42 thousand greater than the median household income at D-rated facilities.

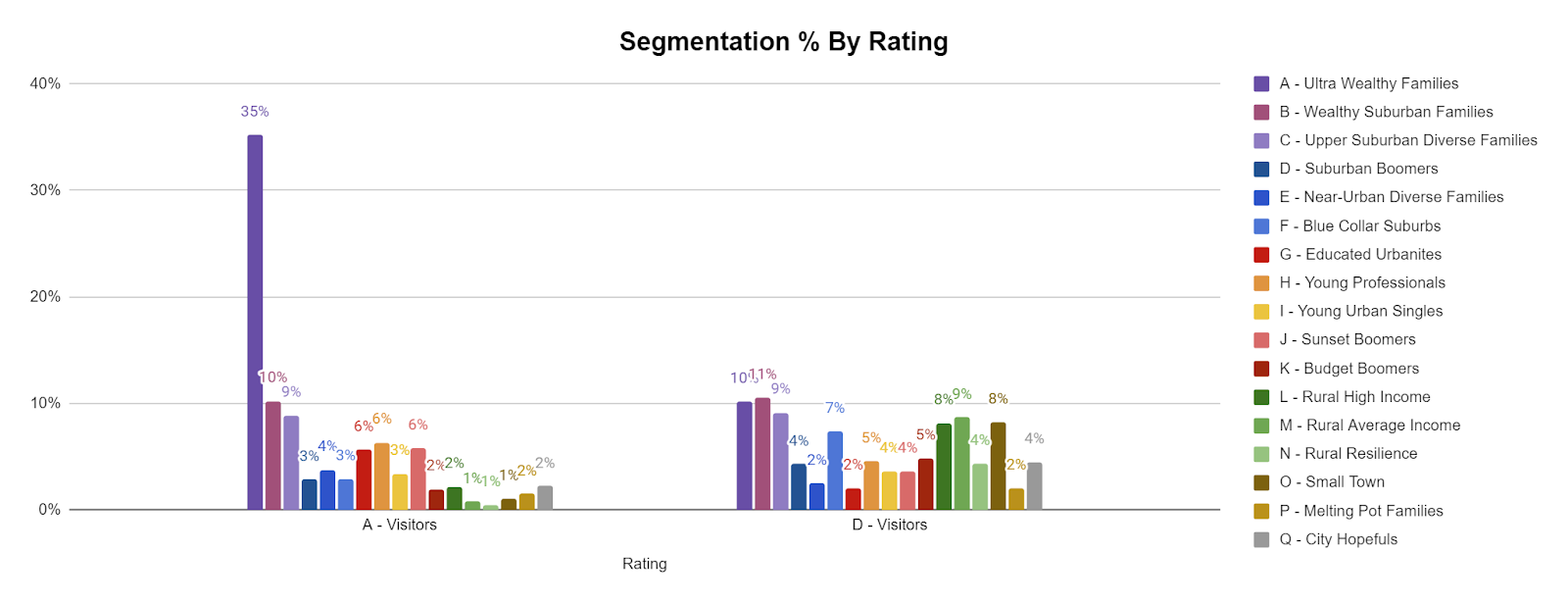

We have also used Spatial.ai’s PersonaLive segmentation to determine the primary segments of visitors to each facility type. A-rated facilities are significantly less diverse, with more than 54% of visitors belonging to the three wealthiest segments – Ultra Wealthy Families, Wealthy Suburban Families, and Upper Suburban Diverse Families. Meanwhile, D-rated facilities are extremely diverse, with the top three segments making up less than 30% of visitors and six segments making up the top 50% of visitors.

How We Can Put Placer.ai to Work for Your Brand

Movement data extends far beyond the golf industry. It can be collected from any location in the United States, including retail spaces, outdoor recreation areas, fitness centers, lodging establishments, dining venues, cities/regions, and residential neighborhoods. We have already used this data to analyze movement at fitness centers, along bike paths, and in hotels to help businesses enhance their operations, boost traffic, and create more targeted marketing campaigns.

Additionally, the platform offers the powerful capability of appending personas and segmentation data to an existing marketing database. With just names, email addresses, physical addresses, and/or zip codes, we can supplement and analyze segmentation data and integrate targeted segments directly into digital platforms such as Meta and X. This enhances ROI by targeting lookalike audiences of your top customers and expands movement data insights to companies without physical locations.

Movement data represents a powerful tool for businesses, helping to create marketing efficiencies and uncover invaluable insights. By embracing this data-driven approach, we can not only enhance our service offerings but also stay competitive in an increasingly data-centric world. As technology continues to evolve, the possibilities for applying movement data will only expand, promising a future where experiences are more personalized, efficient, and enjoyable.